Why your insurance might deny a water damage claim in your East Side home

Water damage in your East Side home can happen in seconds but recovering financially often takes months. Insurance companies deny claims for specific technical reasons that most homeowners never see coming. Understanding these denial patterns before you file could save you thousands of dollars and weeks of frustration.. Read more about The best smart water leak detectors for older homes in the East Side.

The East Side’s historic architecture creates unique vulnerabilities. Many homes built before 1940 have original plumbing systems with galvanized pipes that corrode from the inside out. These gradual failures often get denied as “maintenance issues” rather than covered accidents. Your insurance adjuster will look for signs of long-term neglect that point to gradual damage rather than sudden discharge. Protecting Your Historic Fox Point Home from Water Damage and Mold.

Rhode Island’s freeze-thaw cycles compound these problems. When temperatures swing from 20°F to 50°F in 48 hours, as they often do in Providence winters, pipes expand and contract. This stress weakens joints over time until they fail catastrophically. But if your claim shows signs of corrosion or previous minor leaks, insurers may argue the damage was inevitable regardless of the final trigger. Rhode Island Department of Business Regulation.

The good news is that many denials can be overturned with proper documentation and expert testimony. A professional restoration assessment can prove whether damage was truly sudden and accidental or the result of long-term deterioration. This distinction often determines whether you receive a full payout or nothing at all. Professional Mold Removal and Remediation Services for East Side Homeowners.

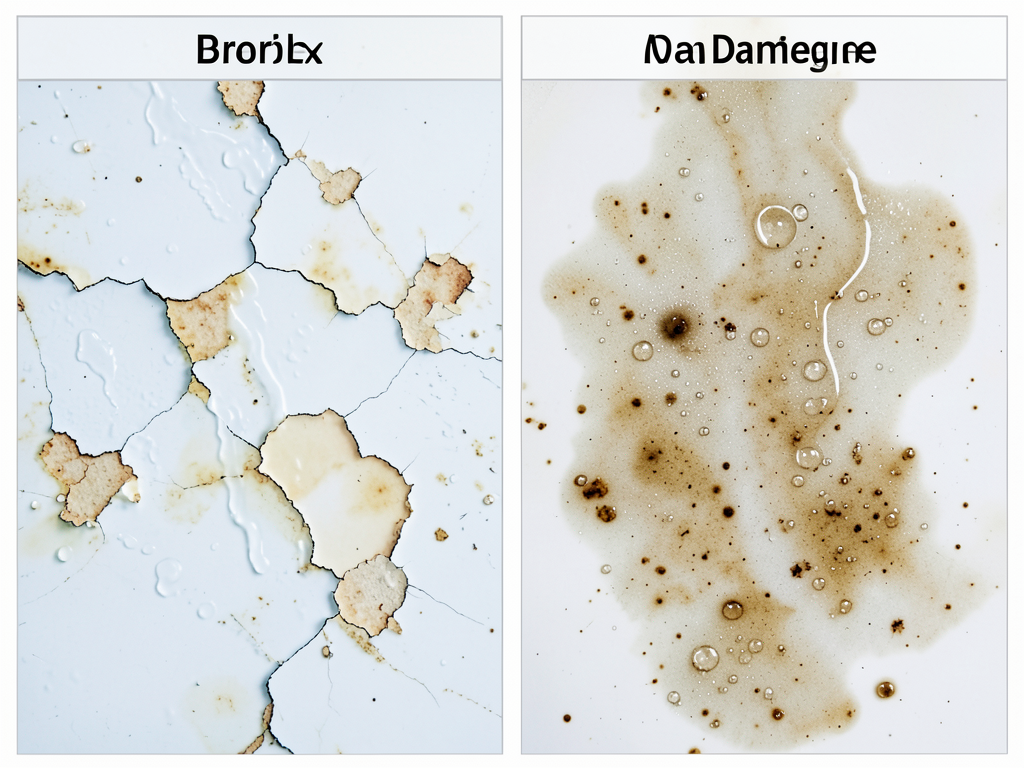

Understanding the ‘Gradual Damage’ Exclusion

Insurance policies specifically exclude damage that happens slowly over time. This “gradual damage” clause is the number one reason claims get denied in Providence. The distinction between sudden and gradual damage often comes down to microscopic evidence that only a trained eye can spot.. Read more about Protecting your East Side home from water damage while you travel for the winter.

Water leaves characteristic patterns as it moves through building materials. A sudden burst pipe creates a clean, uniform moisture pattern with minimal staining. Gradual leaks show concentric rings of mineral deposits, discoloration, and material degradation. Insurance adjusters are trained to spot these differences immediately. Get Immediate 24/7 Emergency Water Extraction in Downtown Providence.

In East Side homes, this becomes critical because many have original plaster walls and hardwood flooring. Water seeping through these materials for months or years creates irreversible damage that looks different from clean water exposure. The adjuster will examine the wood grain for warping patterns and check plaster for efflorescence – that white powdery residue that indicates long-term moisture exposure.. Read more about Who is responsible for water damage in a College Hill off-campus apartment?.

The 48-hour rule also applies here. Insurance companies expect homeowners to address water issues quickly. If you knew about a leak for weeks before filing a claim, they may argue you contributed to the damage by not acting sooner. This is especially true for mold growth, which can establish in 24-48 hours in Providence’s humid climate.

Maintenance Negligence vs. Accidental Discharge

Your insurance covers accidental discharge – pipes that suddenly burst without warning. It does not cover damage from poor maintenance or known problems you failed to fix. This distinction becomes murky in older East Side homes where plumbing systems are near the end of their lifespan.

Common scenarios that trigger maintenance negligence denials include: ignoring a slow drip under the sink for months, knowing about a toilet that rocks on its base, or failing to replace a water heater that’s past its expected service life. Insurance companies argue these are foreseeable problems you should have addressed.

Rhode Island’s building code requires specific maintenance standards for rental properties in Providence. If you’re a landlord on the East Side, your insurance company may hold you to these standards when evaluating claims. Failing to meet code requirements for things like proper drainage or updated plumbing can void coverage entirely.

The “known loss” doctrine also applies. If you knew about a problem before purchasing your policy, or if damage existed before the loss occurred, your claim may be denied. This is why timing matters – filing claims immediately after discovering damage rather than waiting weeks or months.

Flood vs. Water Damage: The Crucial Distinction

Standard homeowners insurance covers water damage from internal sources but excludes flooding from external sources. This distinction trips up many East Side homeowners after heavy rains or snowmelt events.

Flood damage occurs when water enters your home from outside – through windows, doors, or foundation walls. This includes rising groundwater, storm surge, and overflow from rivers or drainage systems. The National Flood Insurance Program (NFIP) defines flood as a general and temporary condition of partial or complete inundation of normally dry land. National Flood Insurance Program.

Providence’s combined sewer overflow system creates unique challenges. During heavy rainfall, the system can back up into basements through floor drains or sump pits. This is technically “sewer backup” rather than flood damage, but it requires a specific endorsement on your policy. Without this coverage, you could face a complete denial even if water entered through no fault of your own.

The Seekonk and Providence Rivers’ proximity to the East Side also matters. Properties within the designated floodplain face different underwriting standards and may need separate flood policies. FEMA’s flood maps show many East Side areas as high-risk zones, especially properties near India Point Park or along the waterfront.

Rhode Island Specific Insurance Factors

Rhode Island insurance regulations create specific requirements that affect claim outcomes. The Rhode Island Department of Business Regulation oversees insurance practices and mandates certain disclosures that can impact your coverage.

Sewer backup endorsements are particularly important in Providence. The city’s aging infrastructure means many homes are vulnerable to backups during heavy rainfall. This endorsement typically costs $50-100 annually but can save you from a $10,000+ loss if your basement floods from a backed-up sewer line.

Rhode Island follows the “efficient proximate cause” doctrine for weather-related claims. This means if wind damages your roof and then rain enters through the damaged area, the wind claim covers the resulting water damage. But if the roof was already in poor condition, the insurance company may deny the claim as maintenance negligence.

The state also has specific requirements for mold remediation coverage. Rhode Island law requires insurers to cover mold damage if it results from a covered water loss. However, they can exclude mold that develops from ongoing humidity or poor ventilation – common issues in East Side homes with old windows and inadequate insulation.. Read more about Why your window wells are filling with water during heavy Providence rainstorms.

Step-by-Step: What to Do After a Denial

Receiving a claim denial doesn’t mean you’re out of options. Many denials get overturned through proper documentation and expert intervention. The key is acting quickly while evidence remains fresh.

First, request a complete copy of your claim file including all photos, moisture readings, and the adjuster’s report. Rhode Island insurance law requires insurers to provide this information within 30 days of your request. Review these documents for errors or omissions that could support your appeal.

Next, document the current condition of all damaged areas. Take date-stamped photos showing the extent of damage, any visible water lines, and the condition of surrounding materials. This documentation becomes crucial if you need to prove the damage was sudden rather than gradual.

Consider hiring a professional restoration company to conduct an independent assessment. Companies certified by the IICRC (Institute of Inspection Cleaning and Restoration Certification) can provide detailed reports on water category, migration patterns, and damage timelines. This technical evidence often carries more weight than homeowner testimony.

Finally, understand your appeal rights under Rhode Island law. You typically have 60 days to appeal a denial, and you can request an independent appraisal if you and your insurer disagree on the damage value. Some denials also qualify for external review through the state insurance department.

Preventing Future Claim Denials

Prevention is always better than appeal when it comes to insurance claims. Regular maintenance and documentation can significantly reduce your risk of denial for legitimate losses.

Schedule annual plumbing inspections for older East Side homes. A licensed plumber can identify corrosion, weak joints, and potential failure points before they cause catastrophic damage. Keep these inspection reports with your insurance documents as proof of proactive maintenance.

Install water leak detection systems that can alert you to problems before they escalate. Many modern systems connect to your smartphone and can automatically shut off water when leaks are detected. Insurance companies increasingly offer premium discounts for these preventive measures.

Document all repairs and upgrades to your plumbing and roofing systems. Keep receipts, permits, and contractor information organized. This paper trail proves you’ve maintained your property properly and can counter arguments about negligence if a claim is disputed.

Understand your policy’s specific exclusions and limitations. Many East Side homeowners discover too late that their policy excludes certain types of water damage or has low sub-limits for mold remediation. Knowing these details helps you make informed decisions about additional coverage.

Secondary Damage and the 48-Hour Window

Time becomes your enemy after water intrusion. Secondary damage – particularly mold growth – can begin within 24-48 hours in Providence’s humid climate. Insurance companies expect you to mitigate damage quickly, and failure to do so can result in claim denial.

Mold requires moisture, organic material, and the right temperature to grow. Providence’s average humidity of 70% creates ideal conditions for mold once water is introduced. Even clean water from a broken pipe can become a mold problem if not addressed within two days.

The “duty to mitigate” clause in most policies requires you to take reasonable steps to prevent further damage. This means stopping the water source, removing standing water, and beginning the drying process. Failure to mitigate can reduce your claim payment or result in complete denial.

Professional restoration companies use specialized equipment to detect hidden moisture that homeowners often miss. Thermal imaging cameras can identify water behind walls, and moisture meters can measure water content in building materials. This thorough assessment prevents secondary damage that could void your claim.

The Role of Professional Documentation

Professional documentation can make or break your claim. Insurance companies give more weight to reports from certified technicians than to homeowner observations or DIY assessments.

A professional restoration assessment includes detailed moisture mapping, material classification, and damage categorization according to IICRC S500 standards. This standardized approach provides the technical evidence insurance companies expect when evaluating claims.

Moisture readings taken at multiple depths show whether water has migrated beyond visible damage. Category 1 water (clean) becomes Category 2 (gray) or Category 3 (black) as it sits and absorbs contaminants. This progression affects both coverage and required remediation procedures.

Professional reports also establish damage timelines. By examining material degradation, mold growth patterns, and water migration, technicians can often determine whether damage occurred suddenly or gradually. This timeline becomes crucial evidence if your claim is disputed.

Common East Side Denial Scenarios

Certain claim types get denied more frequently in East Side homes due to their unique characteristics. Understanding these patterns helps you prepare documentation and set realistic expectations.

Historic home claims often face extra scrutiny. Insurance companies know these properties have aging systems and may look more closely for signs of gradual deterioration. They may also apply different valuation methods for irreplaceable materials like original hardwood or plaster.

Multi-family conversions create additional complications. If your East Side home was converted to a two-family dwelling, insurance companies may argue that unlicensed or unpermitted work contributed to the damage. Always verify your property’s legal use classification with your insurer.

Winter-related claims face particular challenges. Ice dams, frozen pipes, and snow melt all involve complex causation issues. Insurance companies may argue that proper winterization would have prevented the damage, especially in vacant properties during cold snaps.. Read more about How a frozen outdoor faucet can flood your basement in Johnston.

Basement claims in East Side homes often get denied due to pre-existing conditions. Many historic homes have minor foundation cracks or poor drainage that allows occasional moisture intrusion. Insurance companies may argue this pre-existing condition contributed to the claimed damage.

Building a Strong Appeal Case

If your claim is denied, building a strong appeal requires strategic evidence collection and presentation. The goal is to prove your loss meets all policy requirements for coverage.

Start by obtaining all policy documents and reviewing the specific exclusion cited in your denial letter. Many denials result from misunderstandings about coverage rather than actual exclusions. Sometimes a simple clarification can reverse the decision.

Gather independent expert opinions that contradict the insurance company’s assessment. This might include a second restoration company’s evaluation, a plumber’s report on pipe condition, or a building inspector’s findings about structural issues. Multiple expert opinions carry more weight than a single assessment. Finding the Most Reliable Water Damage Restoration Experts in Providence.

Document any communication with your insurance company, including dates, times, and content of conversations. Rhode Island insurance law requires companies to respond to appeals within specific timeframes. If they miss these deadlines, you may have grounds for complaint with the state insurance department.

Consider hiring a public adjuster who works on your behalf rather than the insurance company’s. These professionals understand claim valuation and can often negotiate significantly higher settlements than homeowners achieve on their own. They typically work on contingency, taking a percentage of the recovered amount.

When to Call a Professional

Knowing when to involve professional help can save you time and money. Some situations clearly warrant expert intervention, while others might be handled through direct communication with your insurer.

Call a professional immediately if you notice any of these red flags: the insurance company disputes the cause of damage, they offer a settlement far below your repair estimates, or they cite complex policy exclusions you don’t understand. These situations often require technical expertise to resolve.

Professional help is also crucial if you’re dealing with extensive damage that affects multiple systems in your home. Large claims involve complex valuation issues and may require coordination between various specialists to document the full extent of your loss.

Consider professional intervention if you’re facing a time-sensitive situation. Some denials come with strict appeal deadlines, and navigating the process while managing repairs can be overwhelming. Professionals can handle the administrative burden while you focus on restoring your home.

Remember that early intervention often prevents claim denials. Having a professional assess damage before you file can identify potential issues and help you present your claim in the strongest possible way from the start.

Frequently Asked Questions

Why did my water damage claim get denied if I have insurance?

Most denials occur due to gradual damage exclusions, maintenance negligence, or lack of specific endorsements like sewer backup coverage. Insurance covers sudden, accidental damage but not problems that develop over time or result from poor maintenance.

How long do I have to file an appeal after a claim denial?

Rhode Island law typically gives you 60 days to appeal a denial, but check your specific policy for exact deadlines. Missing these deadlines can permanently bar your right to appeal, so act quickly after receiving a denial.

Can I still get coverage if I’ve had previous water damage?

Yes, but previous damage may affect your claim if it contributed to the current loss. Insurance companies will examine whether the new damage is truly separate or related to unresolved previous issues. Proper documentation of repairs is essential.

What’s the difference between flood and water damage coverage?

Standard homeowners insurance covers internal water damage from plumbing failures but excludes flooding from external sources like rising groundwater or storm surge. You need separate flood insurance through the NFIP for external flooding coverage. Reliable Help for Sump Pump Failures and Flooding in Smith Hill.

How can I prove my damage was sudden and not gradual?

Professional documentation is key. IICRC-certified technicians can provide moisture readings, material analysis, and damage timelines that distinguish sudden from gradual damage. Photos showing clean water lines versus mineral deposits also help prove the damage timing.

Take Action Before It’s Too Late

Water damage in your East Side home requires immediate attention, whether you’re filing a claim or dealing with a denial. Every hour of delay increases the risk of secondary damage that could void your coverage entirely. Don’t let insurance company tactics leave you paying for repairs out of pocket.

Our team understands the unique challenges facing Providence homeowners. We’ve helped countless East Side residents navigate the complex insurance claims process and recover the compensation they deserve. From initial assessment to final documentation, we’re with you every step of the way.

Pick up the phone and call (401) 262-8400 today. Our certified technicians are ready to assess your damage, document your loss, and help you build the strongest possible case for your claim. Whether you’re filing for the first time or fighting a denial, we have the expertise to help you succeed.

Don’t wait until it’s too late. Call (401) 262-8400 now and let us help you protect your East Side home and your financial future. We’re available 24/7 because we know water damage doesn’t wait for business hours.

{

“@context”: “https://schema.org”,

“@type”: “BlogPosting”,

“headline”: “Why your insurance might deny a water damage claim in your East Side home”,

“description”: “Learn why water damage claims get denied in Providence’s East Side. Discover common exclusions, local factors, and what to do next to protect your property.”,

“wordCount”: 2812,

“datePublished”: “2026-05-15T12:24:00.000Z”,

“dateModified”: “2026-05-15T12:24:00.000Z”,

“inLanguage”: “en-US”,

“mainEntityOfPage”: {

“@type”: “WebPage”,

“@id”: “https://atlaswaterdamagerestorationprovidence.com”

},

“publisher”: {

“@type”: “LocalBusiness”,

“name”: “Atlas Water Damage Restoration Providence”,

“url”: “https://atlaswaterdamagerestorationprovidence.com”

},

“author”: {

“@type”: “Organization”,

“name”: “Atlas Water Damage Restoration Providence”,

“url”: “https://atlaswaterdamagerestorationprovidence.com”

},

“image”: {

“@type”: “ImageObject”,

“url”: “https://atlaswaterdamagerestorationprovidence.com/wp-content/uploads/2026/03/why-your-insurance-might-deny-a-water-damage-claim-1.png”

}

}

{

“@context”: “https://schema.org”,

“@type”: “LocalBusiness”,

“name”: “Atlas Water Damage Restoration Providence”,

“url”: “https://atlaswaterdamagerestorationprovidence.com”,

“address”: {

“@type”: “PostalAddress”,

“addressLocality”: “Providence”

},

“areaServed”: {

“@type”: “City”,

“name”: “Providence”

}

}

{

“@context”: “https://schema.org”,

“@type”: “FAQPage”,

“mainEntity”: [

{

“@type”: “Question”,

“name”: “Why did my water damage claim get denied if I have insurance?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Most denials occur due to gradual damage exclusions, maintenance negligence, or lack of specific endorsements like sewer backup coverage. Insurance covers sudden, accidental damage but not problems that develop over time or result from poor maintenance.”

}

},

{

“@type”: “Question”,

“name”: “How long do I have to file an appeal after a claim denial?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Rhode Island law typically gives you 60 days to appeal a denial, but check your specific policy for exact deadlines. Missing these deadlines can permanently bar your right to appeal, so act quickly after receiving a denial.”

}

},

{

“@type”: “Question”,

“name”: “Can I still get coverage if I’ve had previous water damage?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Yes, but previous damage may affect your claim if it contributed to the current loss. Insurance companies will examine whether the new damage is truly separate or related to unresolved previous issues. Proper documentation of repairs is essential.”

}

},

{

“@type”: “Question”,

“name”: “What’s the difference between flood and water damage coverage?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Standard homeowners insurance covers internal water damage from plumbing failures but excludes flooding from external sources like rising groundwater or storm surge. You need separate flood insurance through the NFIP for external flooding coverage. Reliable Help for Sump Pump Failures and Flooding in Smith Hill.”

}

},

{

“@type”: “Question”,

“name”: “How can I prove my damage was sudden and not gradual?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Professional documentation is key. IICRC-certified technicians can provide moisture readings, material analysis, and damage timelines that distinguish sudden from gradual damage. Photos showing clean water lines versus mineral deposits also help prove the damage timing.”

}

}

]

}

{

“@context”: “https://schema.org”,

“@type”: “BreadcrumbList”,

“itemListElement”: [

{

“@type”: “ListItem”,

“position”: 1,

“name”: “Home”,

“item”: “https://atlaswaterdamagerestorationprovidence.com”

},

{

“@type”: “ListItem”,

“position”: 2,

“name”: “Blog”,

“item”: “https://atlaswaterdamagerestorationprovidence.com/blog”

},

{

“@type”: “ListItem”,

“position”: 3,

“name”: “Why your insurance might deny a water damage claim in your East Side home”

}

]

}

{

“@context”: “https://schema.org”,

“@type”: “Service”,

“serviceType”: “Water Damage Restoration”,

“provider”: {

“@type”: “LocalBusiness”,

“name”: “Atlas Water Damage Restoration Providence”,

“url”: “https://atlaswaterdamagerestorationprovidence.com”

},

“areaServed”: {

“@type”: “City”,

“name”: “Providence”

},

“description”: “Learn why water damage claims get denied in Providence’s East Side. Discover common exclusions, local factors, and what to do next to protect your property.”

}